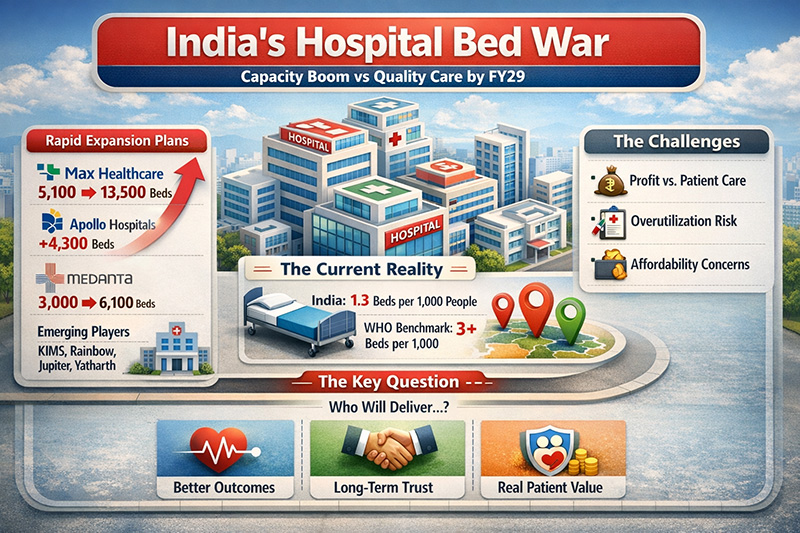

The hospital sector in India is currently experiencing a turning point which is similar to a strategic inflection point. The rapid expansion that has been planned by Max Healthcare, Apollo Hospitals, Medanta, Narayana Health, and Aster DM Healthcare is indicative of far more than simple growth in numbers. Rather, it is a strategic move that marks a transformation of the concept, financing and use of healthcare capacity. The expansion that seems obvious on the surface is actually a calculated “capacity arms race,” and FY29 looks like it could very well shake up India’s leadership among hospitals.

One of the key drivers of change in the hospital industry has long been recognized and under-addressed in India. The country is lacking in hospital bed density, holding less than 1.3 beds for each 1,000 people according to WHO. This number is substantially lower than the recommendation to hold 3 or more. Moreover, the gap has long been mentioned in analyses made in India by NITI Aayog and others. The problem does not lie in a lack of demand; rather, it is the supply problem which is becoming apparent after decades of economic growth in the country.

Thus, the framework used by hospitals in the development of strategies should undergo certain changes. The old approach of being conservative and making investments in assets alone has become inefficient. Hospital beds are now being viewed through the lens of productivity, with indicators such as Average Revenue Per Occupied Bed (ARPOB), occupancy and case-mix index becoming relevant. As Michael Porter and Elizabeth Teisberg explained in Redefining Health Care (Harvard Business School Press, 2006), “value in healthcare is measured by outcomes achieved per dollar spent, not by the volume of services delivered.” At the same time, the focus on quantity could undermine the goal of providing quality healthcare to patients.

Another factor that plays an important role is the practice of land banking. Making such purchases in FY26 can be viewed as a pre-emptive step towards dominance in the market by FY29. This approach correlates with global trends where companies buy out land assets for future development before others realize their potential. For instance, this is what hospital groups have been doing in the USA and in Southeast Asia. However, there are serious questions regarding ethics in light of existing socioeconomic and geographical disparities in the accessibility of medical care.

An important characteristic of the current development of the hospital sector can be attributed to its geographical shift. Cities of tier two and three levels have become the next frontier. Studies in journals such as The Lancet suggest that for India to ensure equal healthcare distribution, there is a need to move towards the decentralization of tertiary care beyond metropolitan centers (Patel et al., 2015). Therefore, the new stage of expansion opens up a lot of opportunities for making healthcare easily accessible and increasing the efficiency of the ecosystem.

Nevertheless, there are many threats related to the new development strategy. If hospitals are trying to expand based mainly on volumes, insurance reimbursements, and occupancies, it might result in commoditization of healthcare in India. The risk is not theoretical because research conducted internationally shows that oversupply can result in increased utilization of interventions without the corresponding benefits (OECD, 2008).

Healthcare thinkers from India have warned against this approach on multiple occasions. For example, Dr. Devi Shetty, the founder of Narayana Health group, emphasizes that the “primary goals of healthcare must be affordability, scalability, and outcomes, not profits.” Likewise, global discussions on health care emphasize the significance of building trust rather than scaling up.

Thus, the ongoing battle of the hospital companies for a greater market share is twofold. On the one hand, it allows overcoming existing bottlenecks and stimulating further economic growth in the country. On the other hand, it entails significant risks of shifting the focus to the commercial aspect rather than quality and patients’ needs.

Strategically, the question now is not whether to expand or not. It is about the direction of the development and whether the expansion will bring actual benefits to patients. As noted by Michael Porter, “the only way to contain costs and improve quality is to improve value.” In the case of India, the issue has become existential.

Dr. Prahlada N.B

MBBS (JJMMC), MS (PGIMER, Chandigarh).

MBA in Healthcare & Hospital Management (BITS, Pilani),

Postgraduate Certificate in Technology Leadership and Innovation (MIT, USA)

Executive Programme in Strategic Management (IIM, Lucknow)

Senior Management Programme in Healthcare Management (IIM, Kozhikode)

Advanced Certificate in AI for Digital Health and Imaging Program (IISc, Bengaluru).

Senior Professor and former Head,

Department of ENT-Head & Neck Surgery, Skull Base Surgery, Cochlear Implant Surgery.

Basaveshwara Medical College & Hospital, Chitradurga, Karnataka, India.

My Vision: I don’t want to be a genius. I want to be a person with a bundle of experience.

My Mission: Help others achieve their life’s objectives in my presence or absence!

My Values: Creating value for others.

References:

- World Health Organization. Global Health Observatory Data Repository.

- NITI Aayog. Health System for a New India: Building Blocks. Government of India.

- Porter ME, Teisberg EO. Redefining Health Care. Harvard Business School Press; 2006.

- Patel V, et al. “Universal health coverage in India.” The Lancet. 2015.

- OECD. Health at a Glance Reports (various years).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Dear Dr. Prahlada N. B Sir,

India's healthcare expansion is indeed a moral imperative, requiring a delicate balance between scale and quality. As the country moves towards bridging the deficit of 1.3 beds per 1,000 people, the focus should shift from mere infrastructure growth to ensuring empathy and quality in care.

To achieve this, integrating three core pillars is crucial:

– *Value-Driven Metrics*: Prioritizing patient-reported outcome measures (PROMs) over Average Revenue Per Occupied Bed (ARPOB)

– *The Shetty Model*: Embracing radical affordability and scalability for world-class outcomes

– *Technological Equity*: Leveraging digital health for equitable diagnostic capabilities across rural and urban centers

The goal is to create a healthcare ecosystem that grows better, not just larger, with trust and patient-centricity at its core.

We should ensure that healthcare expansion benefits marginalized communities &, modern technology should play a vital role in bridging the urban-rural healthcare divide.

Reply