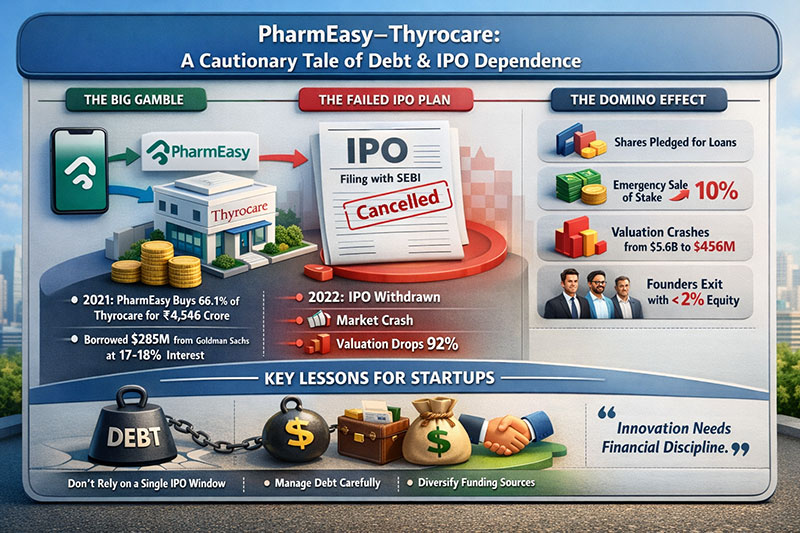

In 2021, PharmEasy was one of the most acclaimed digital health startups in India. Founded by Dharmil Sheth and his childhood friends from Ghatkopar in Mumbai, India, it had grown into India’s largest e-pharmacy platform in no time. Significant investments were made in venture capital as well. At its peak during the startup revolution in India, PharmEasy was valued at around $5.6 billion.

In 2021 itself, PharmEasy made another strategic decision to acquire 66.1% of Thyrocare Technologies Ltd., one of India’s largest and most successful chains of diagnostic centers. It was valued at ₹4,546 crore. It was believed that with this acquisition, PharmEasy would be able to create a comprehensive healthcare ecosystem for its customers by combining its e-pharmacy capabilities with diagnostic services. However, in no time at all, it became another example of how debt-fueled expansion and excessive dependence on capital markets can prove to be detrimental for startups in India.

For its acquisition of Thyrocare Technologies Ltd., PharmEasy had borrowed $285 million from Goldman Sachs at an estimated rate of around 17-18%. Its debt servicing would come to around ₹450 crore every year, irrespective of the fact that its business was not profitable. Its plan of repaying its loan was entirely dependent on its IPO of ₹6,250 crore.

In November 2021 itself, PharmEasy had filed its Draft Red Herring Prospectus with the Securities and Exchange Board of India (SEBI). However, in 2022, with global technology valuations declining significantly due to rising global interest rates and changing investor sentiment, the IPO window was closed for PharmEasy.

Without access to capital via an IPO, the financial structure has remained under significant duress. Reports suggest that the company has mortgaged its own shares of Thyrocare, has sold part of its own holding to raise cash, and has witnessed its valuation fall from multi-billion-dollar valuations to a significantly lower number. Perhaps in one of the more stark examples of this, founders have had to leave with only a minuscule amount of equity in the business they built.

This is an example of a larger concept within corporate finance, which states that capital structures dependent on a single event are systemically risky. Nobel Prize winner Robert Shiller has argued that markets can often be subject to increased levels of both optimism and pessimism and therefore should be avoided as a means of timing business decisions, which can have catastrophic effects on highly leveraged businesses (Shiller, Irrational Exuberance, Princeton University Press, 2000).

Strategic Analysis

Strategically, there is little which is fundamentally flawed in the PharmEasy-Thyrocare deal. The model of integrating pharmacy and diagnostics is one which has long been recognized as an effective model around the globe. In fact, within the United States, companies such as CVS Health have attempted to do exactly this, integrating pharmacy and diagnostics with insurance services. The only difference here is the financial model; whereas companies within the healthcare space have diversified revenue streams and debt structures, PharmEasy has relied on a single event.

Within the Indian business environment, there are perhaps more lessons which can be learned. For example, Ratan Tata has long stated, “I don’t believe in taking right decisions. I take decisions and then make them right.” This is perhaps more likely to be effective when there is financial flexibility available.

Similarly, global investors often place significant emphasis on sustainable capital strategy. Warren Buffett has incisively commented, “Only when the tide goes out do you discover who’s been swimming naked.” The fall in global tech valuations in 2022 has shown that many startups’ growth is based on assumptions related to market conditions rather than economic fundamentals.

For India’s booming startup market, there are significant implications to be learned from PharmEasy’s story. The Indian market is witnessing an unprecedented trend of venture-backed companies gearing up to list their companies. Industry reports have shown that many startups have recently filed draft prospectus documents with regulators. Although this is an encouraging trend in India’s entrepreneurial ecosystem, it also highlights the need to develop financial architectures.

One of the key learnings is related to diversifying financial routes. Startups that have adopted venture capital and operational profitability, along with strategic partnerships and moderate debt, are more likely to withstand market timing risks. Another significant financial route is related to debt and interest rates.

Thus, PharmEasy’s story should not be seen as an outright business failure but rather as part of India’s digital health market evolution story. Ambitious entrepreneurs will continue to explore new routes and acquisitions and look to integrate businesses; however, long-term sustainability is more likely to be achieved by those entrepreneurs who balance business aspirations with financial sustainability.

Thus, as India’s startup market grows and matures, it is possible to articulate another significant financial route as follows: innovation is necessary for business growth; financial sustainability is necessary to sustain business growth.

Dr. Prahlada N.B

MBBS (JJMMC), MS (PGIMER, Chandigarh).

MBA in Healthcare & Hospital Management (BITS, Pilani),

Postgraduate Certificate in Technology Leadership and Innovation (MIT, USA)

Executive Programme in Strategic Management (IIM, Lucknow)

Senior Management Programme in Healthcare Management (IIM, Kozhikode)

Advanced Certificate in AI for Digital Health and Imaging Program (IISc, Bengaluru).

Senior Professor and former Head,

Department of ENT-Head & Neck Surgery, Skull Base Surgery, Cochlear Implant Surgery.

Basaveshwara Medical College & Hospital, Chitradurga, Karnataka, India.

My Vision: I don’t want to be a genius. I want to be a person with a bundle of experience.

My Mission: Help others achieve their life’s objectives in my presence or absence!

Leave a reply

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a reply