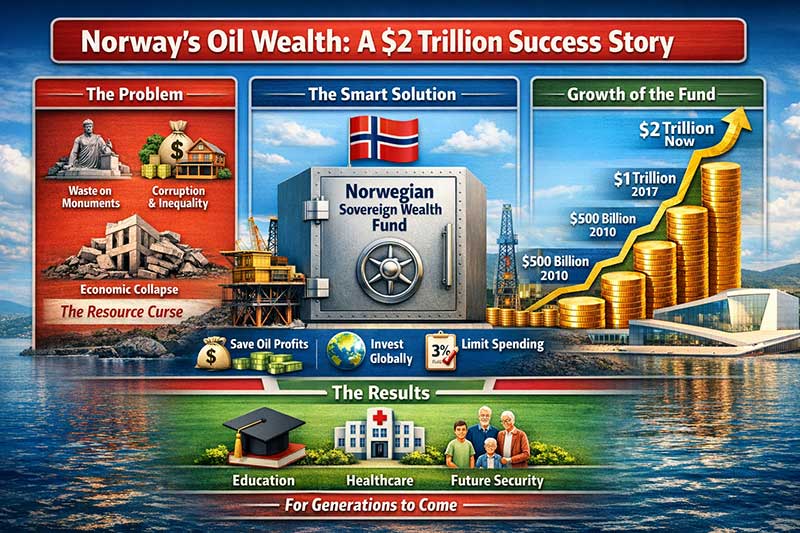

The discovery of the Ekofisk oil field by Norway in 1969 was a watershed not only for the Norwegian economy but for the entire world in terms of resource management. Many countries around the world have been victims of what economists call the “resource curse” or “paradox of plenty,” which refers to the tendency for countries with an abundance of resources to experience corruption and economic instability instead of prosperity and economic growth. For example, Nigeria and Venezuela are two countries whose economies have been plagued by the so-called resource curse. Nigeria has been a victim of corruption and underdevelopment despite having an abundance of oil resources, while Venezuela has been plagued by economic ruin due to the fall of oil prices (Sachs & Warner, 2001; Ross, 2012). In light of these issues, the Norwegian model stands out as a shining example of good governance and statesmanship.

In 1990, the Norwegian Parliament established the Government Pension Fund Global (GPFG), a sovereign wealth fund whose objective was to convert finite oil wealth into perpetual wealth for the Norwegian people. Unlike many countries whose economies have been ruined by the resource curse, Norway decided not to squander the windfall gains from oil prices. Instead, the Norwegian Parliament decided to invest the windfall gains globally. In short, the Norwegian Parliament established a simple yet revolutionary principle: only a small percentage of the windfall gains, capped at 4% and later reduced to around 3%, would be used annually for the Norwegian budget while the rest would be saved for generations yet unborn. As the Norwegian Ministry of Finance has repeatedly stated: “The fund is a savings vehicle for future generations” (Norwegian Ministry of Finance, 2023).

The end result has been phenomenal. The GPFG has risen from its original deposit of $150 million in 1996 to more than $1.5-2 trillion today, making it the world’s largest sovereign wealth fund (Norges Bank Investment Management, 2024). Significantly, more than half of that amount has come not from its oil revenues but from its investment returns. By spreading its investments across thousands of global corporations, bonds, and properties, Norway has, in effect, converted its non-renewable natural wealth into a diversified, renewable financial wealth. As economist Elroy Dimson explains, “long-term investing, diversification, and discipline are the key drivers of sovereign wealth success” (Dimson et al., 2021).

From an advocacy perspective, Norway’s sovereign wealth fund is significant for several reasons. As Kofi Annan, former UN Secretary-General, once noted, “good governance is perhaps the single most important factor in eradicating poverty and promoting development.” The governance structure that Norway established, where transparency, ethical investment, and political consensus were paramount, ensured that short-term political considerations did not compromise long-term national interest. This is especially compared to other resource-rich nations where short-term political considerations compromise long-term sustainability.

India provides an interesting case study. India is not an oil-rich country like Norway. However, India is facing the same challenge of effectively utilizing public resources, be it from taxation, oil reserves, or the proceeds of disinvestments. India’s Economic Survey has repeatedly emphasized the need for fiscal responsibility and capital formation. Raghuram Rajan, the former RBI Governor of India, has cautioned India about the need for sustainable growth: “Sustainable growth requires institutions that resist the temptation of short-term populism.” India and other emerging economies may learn from Norway’s experience of setting up institutions to utilize strategic resources.

However, there are some limitations of Norway’s model as well. One of the limitations of Norway’s model is that it might not allow for sufficient social spending in the present, especially in countries where development is a pressing need. It is not always possible for developing countries to wait and save, especially when a large portion of their population is not receiving basic amenities and services. Moreover, Norway was also able to achieve this because of its strong institutions, lack of corruption, and small population size, which might not always be feasible for every country. According to political economist Terry Lynn Karl, “institutions determine whether resources become a curse or a blessing” (Karl, 1997).

Besides, there are also some ethical and geopolitical issues involved in Norway’s model as well. The investments of Norway’s fund are not just made domestically, and they also include companies that might be involved in some of the more controversial sectors of the economy. Even though Norway has established some ethical investment guidelines and has also made some divestment policies, there is still some debate about the ethical implications of such investments made by Norway. Moreover, investing in global markets also puts Norway at risk of economic volatility.

Yet, in spite of these challenges, the Norwegian model offers a highly effective template for sustainable wealth management. It embodies a fundamental ethical truth: that our wealth in natural resources is not our exclusive privilege but our shared inheritance. As the famous Indian philosopher Mahatma Gandhi once said, “The world has enough for everyone’s need, but not for everyone’s greed.” Norway has concretized this philosophy in practice at the national level by choosing to manage rather than consume its wealth.

The true brilliance of the Norwegian model was not in discovering oil in the first place, but in fighting the human and political instinct to spend it. By incorporating ethics and sustainability into the very framework of their economic system, Norway has secured its future beyond its resources. In a world of climate risk and economic stress, the Norwegian model offers a strong rationale for nations to look beyond the next election and invest in the future citizens they may never know.

Dr. Prahlada N.B

MBBS (JJMMC), MS (PGIMER, Chandigarh).

MBA in Healthcare & Hospital Management (BITS, Pilani),

Postgraduate Certificate in Technology Leadership and Innovation (MIT, USA)

Executive Programme in Strategic Management (IIM, Lucknow)

Senior Management Programme in Healthcare Management (IIM, Kozhikode)

Advanced Certificate in AI for Digital Health and Imaging Program (IISc, Bengaluru).

Senior Professor and former Head,

Department of ENT-Head & Neck Surgery, Skull Base Surgery, Cochlear Implant Surgery.

Basaveshwara Medical College & Hospital, Chitradurga, Karnataka, India.

References:

- Sachs JD, Warner AM. Natural resources and economic development: The curse of natural resources. Eur Econ Rev. 2001.

- Ross ML. The Oil Curse: How Petroleum Wealth Shapes the Development of Nations. Princeton University Press; 2012.

- Norwegian Ministry of Finance. The Government Pension Fund Global – Strategy and Management. 2023.

- Norges Bank Investment Management. Annual Report 2024.

- Dimson E, Marsh P, Staunton M. Triumph of the Optimists: 101 Years of Global Investment Returns. Princeton University Press; 2021.

- Karl TL. The Paradox of Plenty: Oil Booms and Petro-States. University of California Press; 1997.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a reply